I Already Used Stremline Refinance Can I Do It Again

The FHA Streamline Refinance

If you currently have an FHA mortgage, the FHA Streamline Refinance is the easiest manner to become a lower charge per unit and monthly payment.

The FHA Streamline is a "low-doc" refinance with limited paperwork required. The lender doesn't take to verify your income or credit, and in that location'due south no abode appraisal.

That ways a Streamline Refinance closes faster than other loans and has slightly cheaper closing costs.

Thanks to the FHA Streamline, borrowers with FHA loans take easier access to today's low rates than almost other homeowners.

In this article (Skip to…)

- About the FHA Streamline

- FHA Streamline rates

- How it works

- Types of Streamline Refi

- FHA Streamline benefits

- Are you eligible?

- FHA MIP cancellation

- Streamline vs cash-out refi

- FHA Streamline FAQ

What is the FHA Streamline Refinance loan?

The FHA Streamline is a special refinance program reserved for homeowners with existing FHA mortgages. An FHA Streamline is the fastest, simplest way for FHA-insured homeowners to refinance their mortgages at today'southward low mortgage rates.

Benefits of the FHA Streamline plan include:

- Low refinance rates: FHA loan rates currently average % (% Apr).* This is a low charge per unit compared to much of the mortgage industry

- Lower MIP rates: If y'all got an FHA loan between 2010 and 2015, you can admission today's lower annual mortgage insurance premiums using FHA streamline refinancing

- MIP refund: Homeowners who utilize the FHA Streamline Refinance may be refunded up to 68% of their prepaid mortgage insurance, in the form of an MIP disbelieve on the new loan

- No appraisal: You could employ the FHA Streamline Refinance fifty-fifty if your electric current mortgage is underwater

- No verification of task or income: You may exist eligible for FHA Streamline refinancing even if you recently lost your task or took a pay cut

- No credit check: A low credit score won't stop yous from using the FHA Streamline'south non-credit qualifying choice. This is almost impossible to find with other refinance loans

If you have an existing FHA loan and you want to refinance into a lower interest rate, the FHA Streamline should be your first terminate. Its benefits are nearly unmatched by any other refinance selection.

*Interest rates updated daily according to The Mortgage Reports' lender network. Run into our full rate assumptions hither

FHA Streamline Refinance rates

Today's average 30-twelvemonth FHA rate is % (% APR) co-ordinate to our lender network. Only retrieve, the FHA mortgage insurance fee adds 0.85% in annual costs. This also applies to Streamline Refinances.

Today'due south FHA refinance rates, May twenty, 2022

| xxx-Year FHA Stock-still Rate | % (% Apr) |

| 15-Year FHA Stock-still Rate | % (% Apr) |

| 30-Year Conventional Rate | % (% APR) |

| 15-Year Conventional Rate | % (% Apr) |

Involvement rates are for example purposes only. Your own rate will vary. See our rate assumption here .

How the FHA streamline works

For the most part, the FHA Streamline works like any other refinance product. You take out a new FHA mortgage — typically with a improve interest charge per unit and lower monthly payment — which replaces your existing loan. Your current mortgage must be FHA-backed to utilize this plan.

The FHA Streamline is available as a fixed-rate or adjustable-charge per unit mortgage; information technology comes with a xv- or 30-year term; and there's no FHA prepayment punishment to worry nigh.

Note that the FHA Streamline cannot be used to refinance a 30-year mortgage into a 15-year mortgage.

It can, however, be used to extend a 15-year loan into a xxx-year loan. Doing this lowers monthly payments fifty-fifty further for homeowners. But information technology also stretches out your interest payments, which ways you could pay more in the longer term.

Some other big benefit is that rates for the FHA Streamline Refinance are the same as FHA home purchase rates. There's no penalty for beingness underwater, or for having very picayune equity.

FHA Streamline Refinance pros & cons

| FHA Streamline Refinance Pros | FHA Streamline Refinance Cons |

| Easy to authorize, especially with not-credit qualifying pick | No cash-back allowed |

| Access today's lower involvement rates | Some lenders have stricter rules (so store effectually!) |

| Lower MIP rates for some borrowers | You can't shorten your loan term |

| No home appraisal necessary | Closing costs tin't be rolled into the loan balance |

Types of FHA Streamline Refinance loans

The Federal Housing Assistants offers two different Streamline Refinance options:

- Credit-Qualifying Streamline Refinance: Lenders will check your credit score and debt-to-income ratio to see whether you lot'd be able to brand the loan'south payments

- Not-Credit Qualifying Streamline Refinance: Lenders can approve this refinance without checking your credit score or verifying your income. This is the most common option

Why would anyone cull the credit qualifying option and go through the full underwriting process?

Well, there are times when credit qualifying is necessary — similar when you're adding a new co-borrower to the loan or removing an existing co-borrower.

In other cases, qualifying for the loan all over once more could save you money. If your credit contour has improved a lot since you got your original loan, you might qualify for an fifty-fifty better involvement rate, for example.

What documents do I demand for an FHA Streamline Refinance?

The FHA Streamline Refinance is a "depression-doc" refinance loan, meaning information technology requires less paperwork than most other mortgages. But you'll all the same need some documentation, including:

- A loan application

- A electric current mortgage statement showing a 6-month payment history

- Contact information for your employer (the lender may verify employment, simply not income)

- Two months' worth of banking concern statements showing yous tin can cover out-of-pocket closing costs

- Utility bills showing you lot utilize the home as a primary residence

If y'all apply the FHA's credit-qualifying Streamline Refinance, you lot volition need to "re-qualify" with your income and credit score. This option would exist required if you're removing a co-borrower from the loan.

FHA Streamline Refinance benefits

Nosotros've already mentioned that the FHA Streamline can lower your rate and mortgage payments. But there are other benefits to this refinance programme, too. For example:

- There's no abode appraisal required

- Very little documentation is required

- You could get a fractional MIP refund (applies to the new loan's upfront MIP cost)

Permit's dig into each of those a niggling further.

i. No home appraisal

The biggest difference between the FHA Streamline and almost traditional mortgage refinance options is that the FHA Streamline doesn't require a dwelling appraisal.

Instead, the FHA will allow yous to utilise your original purchase cost as your domicile's electric current value, regardless of what your dwelling is really worth today.

In this style, with its FHA Streamline Refinance program, the FHA does non care if you are underwater on your mortgage. Rather, the program encourages underwater refinancing.

Even if y'all owe twice what your home is at present worth, FHA may allow you to refinance your home without added cost or penalty.

The "appraisal waiver" has been a huge striking with U.S. homeowners, assuasive unlimited loan-to-value (LTV) dwelling house loans via the FHA Streamline Refinance program.

2. Reduced documentation

Another large plus is that information technology's adequately piece of cake to go an FHA Streamline Refinance loan, especially the non-credit qualifying blazon.

The non-credit qualifying Streamline Refinance does not crave most of the typical verifications you'd need to go a new mortgage.

Every bit it's written in the FHA's official mortgage guidelines:

- Employment verification is not required with an FHA Streamline Refinance

- Income verification is not required with an FHA Streamline Refinance

- Credit score verification is not required with an FHA Streamline Refinance (though most lenders will bank check credit)

When you put information technology all together, you can:

- Exist out-of-work

- Have no income

- Have a shaky credit report

- Accept no home equity

Notwithstanding, you could all the same potentially be approved for an FHA Streamline Refinance's not-credit qualifying choice.

That'due south not as crazy equally information technology sounds, past the mode.

To empathise why the FHA Streamline Refinance is a smart program for the FHA, we take to recall the FHA's principal role is to insure mortgages — not "make" them.

It's in the FHA's best interest to help as many people as possible qualify for today'due south low mortgage rates. Lower mortgage rates mean lower monthly payments which, in theory, leads to fewer loan defaults.

This is good for homeowners who want lower mortgage rates, and it's good for the FHA. With fewer loan defaults, the FHA has to pay fewer insurance claims to lenders.

In short, the FHA is helping itself when it helps y'all, which is why the requirements for the Streamline refi are so lenient.

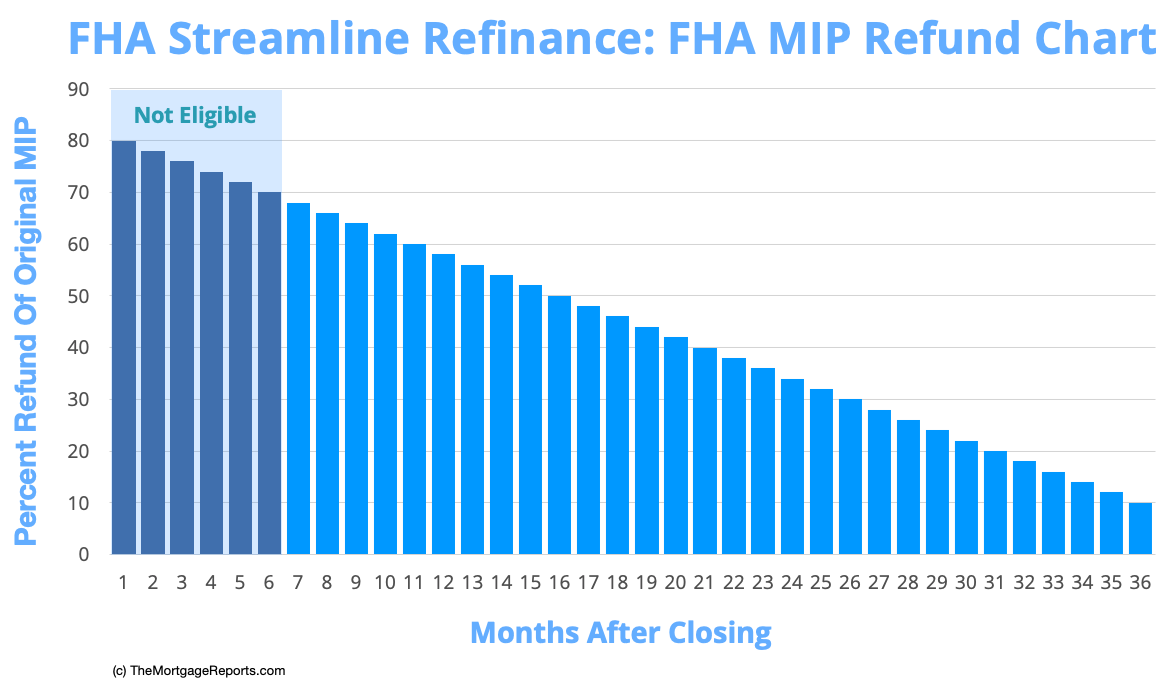

three. FHA MIP refund

There's an additional benefit for FHA-backed homeowners refinancing within the first three years of their existing loan origination.

The FHA provides a partial refund on the upfront mortgage insurance premium (UFMIP) you paid when you first got your FHA loan.

The size of the refund diminishes every bit the three-year window elapses.

For example, a homeowner who refinances an FHA mortgage afterwards xi months is granted a 60% refund on their initial FHA UFMIP.

Thirty days later, the refund drops to 58%. Later on another xxx days, it drops to 56%, then on.

| Months After Closing | MIP Refund | Months After Closing | MIP Refund | Months After Endmost | MIP Refund |

| seven | 68% | 17 | 48% | 27 | 28% |

| 8 | 66% | 18 | 46% | 28 | 26% |

| 9 | 64% | 19 | 44% | 29 | 24% |

| ten | 62% | twenty | 42% | thirty | 22% |

| 11 | lx% | 21 | 40% | 31 | twenty% |

| 12 | 58% | 22 | 38% | 32 | 18% |

| thirteen | 56% | 23 | 36% | 33 | 16% |

| fourteen | 54% | 24 | 34% | 34 | 14% |

| 15 | 52% | 25 | 32% | 35 | 12% |

| 16 | l% | 26 | 30% | 36 | ten% |

Note: FHA homeowners are merely eligible for the Streamline Refinance plan later on six months. Thus, eligibility for an MIP refund starts at seven months.

This is why information technology'due south rarely a expert idea to "wait to refinance" an FHA loan.

With the FHA Streamline Refinance programme, the sooner you refinance, the bigger your refund, and the lower your total loan size for your new mortgage.

This lowers the monthly payment and preserves the home equity — two huge positives.

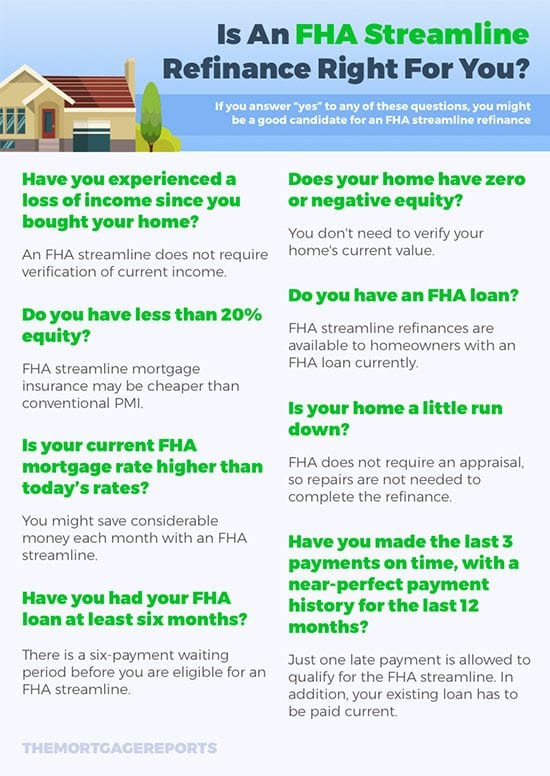

Are yous eligible for an FHA Streamline Refinance?

Although the FHA Streamline Refinance bypasses traditional mortgage standards, like income verification and credit qualifying, the programme does enforce minimum standards for applicants.

You lot'll need to bear witness:

- Three months of on-fourth dimension mortgage payments

- At least 210 days since your home purchase or final refinance

- A clear monetary benefit to refinancing

- That you tin lower your interest charge per unit by at least 0.l% in nigh cases

The official FHA Streamline Refinance guidelines are below. Note that not all mortgage lenders will underwrite to the official guidelines of the Federal Housing Administration.

Some lenders might enforce credit score minimums or other underwriting standards for FHA Streamline mortgages.

If your current lender is requiring a home appraisement or income verification, you're gratuitous to shop effectually for a more than lenient lender that adheres to the FHA's minimum guidelines for Streamline refinancing.

Perfect, 3-month payment history is required

The FHA's main goal is to reduce its overall loan pool take chances. Therefore, its number one qualification standard is that homeowners using the Streamline Refinance plan must accept a perfect payment history stretching back at least three months.

Homeowners with 30-24-hour interval, lx-day, and 90-day belatedly payments are not immune to utilize this refinancing pick.

One tardily mortgage payment is immune in the final 12 months. Loans must be electric current at the time of endmost.

Required 210-day "waiting period" after buying or refinancing

The FHA requires that borrowers brand six on-time mortgage payments on their current FHA-insured loan, and that 210 days pass from the most recent closing date, in order to be eligible for a Streamline Refinance.

The refinance must have a "purpose"

Streamline Refinance applicants must demonstrate a "Net Tangible Benefit" from the refinance, pregnant there will be a clear monetary benefit to the new loan.

Loosely, Net Tangible Benefit is divers equally reducing the "combined charge per unit" by at least one-half of ane per centum.

For instance, say a homeowner has an FHA loan opened in May 2019 with a rate of 4.00%, and an almanac mortgage insurance premium equal to 0.85% of the mortgage amount.

- The combined rate is iv.85%

- The homeowner looks into a Streamline Refinance, and receives a rate quote at 3.25% with MIP of 0.85%

- The new combined charge per unit would exist 4.10%, or three-quarters of ane percent lower than the existing combined rate This FHA refinance would be eligible

Another allowable Net Tangible Benefit is to refinance from an adjustable-charge per unit mortgage to a fixed-rate mortgage.

This is considered a benefit because fixed-rate mortgages accept predictable rates and payments that carry less risk of default.

Taking cash out of your equity is not an commanded Net Tangible Benefit, merely the FHA does have a cash-out refinance loan that we'll discuss below.

Employment and income are not verified

The FHA does not crave verification of a borrower'south employment or annual income as part of the FHA Streamline process, unless the borrower needs a credit qualifying loan.

For non-credit qualifying Streamline loans, there is no verification of employment, nor are there paystubs, Westward-2s, or revenue enhancement returns required for approval.

Credit scores are not verified

The FHA does not verify credit scores every bit part of the FHA Streamline Refinance program, unless you need the credit qualifying option. Instead, it uses payment history as a gauge for future loan performance.

This means that FICO scores below 640, beneath 620, beneath 580, and even below 500 could be eligible for Streamline Refis.

Some lenders, however, create their ain minimum requirements. Cheque your lender's credit qualifying guidelines before applying.

Loan balances may not increase to embrace loan costs

FHA does not permit you lot to roll closing costs into your new loan balance on an FHA Streamline Refinance.

"This is the big negative for most homeowners, as this can become costly," says Jon Meyer, The Mortgage Reports loan expert and licensed MLO.

The maximum mortgage amount on your new loan is equal to your electric current principal balance plus your upfront mortgage insurance premium.

All other costs — including origination charges, championship charges, and prepaid taxes and insurance — must be either paid by the borrower as greenbacks at closing, or credited by the loan officer in full.

The latter is called a "no-cost FHA Streamline." Using this choice, your lender covers the closing costs. But you pay a higher involvement rate in exchange. So you lot'll ultimately pay more over the life of the loan.

No cash-out immune with the FHA Streamline

You can't take extra greenbacks out when refinancing with an FHA Streamline loan. This refinance is designed mainly to lower the homeowner's involvement charge per unit and payment.

However, the FHA cash-out refinance is another refinancing selection offered by the FHA.

Information technology allows y'all to open up a loan of up to 80% of your home's value. If that amount is larger than your current loan balance, y'all take the divergence in cash.

Homeowners tin employ these funds for whatever purpose: to pay off debt, improve your home, or create an emergency fund.

Should you apply the FHA Streamline?

What happens to FHA mortgage insurance if you utilize the Streamline Refinance?

Like other FHA loans, the FHA Streamline Refinance requires borrowers to pay mortgage insurance.

Even if you've built equity in the abode since purchasing information technology, the FHA Streamline Refinance cannot exist used to eliminate mortgage insurance premium (MIP).

FHA borrowers are required to make two types of mortgage insurance payments:

- Upfront Mortgage Insurance Premium (UFMIP) = i.75% of the loan amount added to your loan (not due as cash at closing)

- Annual Mortgage Insurance Premium (MIP) = 0.85% of the loan corporeality split into 12 installments, which are paid with your mortgage each month

This is true for Streamline Refinance loans also as buy loans.

"For borrowers who qualified for an MIP refund, the refund can exist applied toward this total new upfront cost," adds Meyer.

one. Upfront Mortgage Insurance Premium (UFMIP)

Not all refinancing households will pay the full amount of upfront MIP.

Equally shown in the chart above, those using an FHA Streamline within three years of their original loan stand to get an upfront MIP refund.

This can significantly lower the amount of UFMIP added to your new loan and reduce the corporeality y'all have to pay overall.

two. Annual Mortgage Insurance Premium (MIP)

The annual MIP toll for an FHA Streamline Refinance is equally follows:

- 15- & thirty-yr loan terms with an LTV over 90%: 0.85% annual MIP, payable for the life of the loan

- xv- & 30-twelvemonth loan terms with an LTV under 90%: 0.85% almanac MIP, payable for xi years

If you got your existing FHA loan before January 2015, when MIP rates were college, yous could lower your MIP rate with a Streamline Refinance.

The FHA's MIP rules take changed a lot over the years, and the age of your loan will help determine how much you could save.

If your current FHA MIP is higher than what's shown above, consider starting a refinance immediately to benefit from a new, lower FHA MIP.

FHA MIP Cancellation Policy

The FHA requires virtually homeowners to pay mortgage insurance for the life of the loan.

Only homeowners with a starting loan-to-value ratio of xc% or less can abolish mortgage insurance after 11 years. (An LTV of 90% or less means you made at least a 10% down payment.)

Refinancing homeowners could too bring greenbacks to closing to reduce their loan rest and change their MIP disposition. However, non everyone will have the greenbacks to make such a move.

This is why, when exploring an FHA Streamline Refinance, you lot should likewise look at other mortgage refinance options including conventional mortgage loans via Fannie Mae or Freddie Mac.

If y'all tin can qualify for a depression rate, conventional loans have a big plus: You can cancel private mortgage insurance (PMI) one time your loan-to-value ratio falls below eighty%.

The FHA allows its homeowners to refinance to a conventional loan to abolish FHA MIP.

FHA Streamline vs. FHA Cash-Out Refinance

Compared to FHA Streamline Refinance loans, the FHA cash-out refinance has an obvious do good: y'all tin can use it to admission greenbacks from your dwelling disinterestedness.

Say, for example, that you lot owe $250,000 on your current loan but your home is worth $350,000. The difference between these 2 numbers — $100,000 — is your habitation disinterestedness.

With a greenbacks-out loan, you could access part of this disinterestedness while also refinancing your unabridged mortgage. Your loan amount would increase as a effect.

With a Streamline Refinance, your loan corporeality cannot increment to generate cash back, even if you lot do take the equity to dorsum a larger loan.

If you're considering a cash-out refinance instead of a Streamline loan, know that:

- You'll need to qualify with your debt, income, and credit score

- You'll demand a new abode appraisal to verify your habitation's value

- You tin refinance any type of mortgage, not only an FHA loan

- Your loan amount will increment so your annual MIP will, also

- You lot won't be able to access all your equity — only upwards to lxxx%

- Your mortgage rate could increase since greenbacks-out loans are riskier

A Streamline loan is designed for simplicity, so it can contrivance most of the boosted steps cash-out loans require.

FHA Streamline Refinance FAQ

What is the FHA Streamline program?

The FHA Streamline is a refinance program that only current FHA homeowners tin can use. Information technology's faster and easier than most refinance programs, with no documentation required for income, credit, or domicile appraisal. An FHA Streamline Refinance can help homeowners lower their almanac mortgage insurance premium (MIP) or fifty-fifty get a partial refund of their upfront MIP payment. So if you used an FHA loan as a outset-time habitation buyer or repeat buyer, this refi program is designed with you lot in mind.

How does the FHA Streamline Refinance work?

The FHA Streamline Refinance resets your mortgage with a lower interest rate and monthly payment. If you have a 30-year FHA mortgage, you lot can use the FHA Streamline to refinance into a cheaper thirty-yr loan. 15-year FHA borrowers can refinance into a 15- or thirty-year loan. The FHA Streamline does non cancel mortgage insurance premium (MIP) for those who pay it. But annual MIP rates may go down, depending on when the loan was originated.

Do I have to pay closing costs on an FHA Streamline Refinance?

The borrower pays closing costs on an FHA Streamline Refinance. Unlike other types of refinances, y'all cannot roll these costs into your loan amount. FHA Streamline closing costs are typically the same equally other mortgages: 2 to 5 pct of the mortgage amount, which would equal $iii,000 to $7,500 on a $150,000 loan. The difference is that you don't have to pay for an appraisal on an FHA Streamline, which could salvage about $500 to $1,000 in closing costs.

Does an FHA Streamline Refinance get rid of PMI?

No, the FHA Streamline Refinance does not eliminate mortgage insurance. Refinanced FHA loans still have the FHA's annual mortgage insurance, also as a new upfront mortgage insurance fee equal to ane.75 percent of the loan amount. The upfront fee is added to your loan amount. However, if you utilize the FHA Streamline Refinance within 3 years of opening your loan, you lot'll be refunded part of your original UFMIP fee — thus lowering the full mortgage amount.

Who qualifies for an FHA Streamline Refinance?

To qualify for an FHA Streamline Refinance, your current domicile loan must exist insured by the FHA. If you're not certain whether it is, enquire your lender. FHA also requires three months of on-time payments and a 210-day waiting catamenia since your dwelling's concluding closing date (either purchase or refinance). Finally, the FHA Streamline Refinance must have a purpose. That normally ways the refinance needs to lower your combined involvement and insurance rate by at least 0.50 pct.

Does FHA Streamline require a credit check?

Technically, the FHA Streamline does not crave a credit check. That ways homeowners could potentially use the Streamline Refinance even if their credit score has fallen beneath the 580 threshold for FHA loans. However, some lenders may check your credit written report anyway. And so if your credit is on the lower cease, be sure to shop effectually.

Can y'all cash out on an FHA Streamline?

No, you cannot have cash out on an FHA Streamline Refinance.

When tin I do an FHA Streamline Refinance?

FHA homeowners are eligible for a Streamline Refinance 210 days after their last closing. That means you must accept fabricated half-dozen consecutive mortgage payments since you lot purchased or refinanced the domicile.

Tin can I utilize an FHA Streamline twice?

Yep, you can use the FHA Streamline Refinance more than once. You just need to encounter FHA'south guidelines — meaning it's been at least 210 days since your final refinance, you've made your last three payments on time, and you lot can lower your rate at least 0.l pct.

What are the benefits of an FHA Streamline?

The big do good of an FHA Streamline Refinance is that you can switch your FHA loan to a lower charge per unit and monthly payment. You can save coin by getting rid of your existing higher interest rate without as much hassle as traditional refinancing options. Some other benefit of the FHA Streamline is that there'southward no home appraisal – so yous can refinance into a lower FHA mortgage rate fifty-fifty if y'all take very little equity or your loan is underwater.

Is the FHA Streamline Refinance worth it?

The FHA Streamline Refinance is probably worth information technology if you tin lower your mortgage rate and monthly payment a pregnant amount. It's an especially practiced deal for homeowners who purchased or refinanced from 2010 to 2015, because FHA has since lowered its annual mortgage insurance rates. Past refinancing a pre-2015 mortgage with the FHA streamline, you lot may be able to drop your annual mortgage insurance charge per unit from over i per centum to just 0.85 percent.

How practice I get rid of PMI on an FHA loan?

FHA mortgage insurance premium (MIP) lasts 11 years if you made a downwards payment of x percent or more. It lasts the full life of the loan if your downwards payment was less than ten percent. The just way to get rid of FHA mortgage insurance is by refinancing your current FHA loan into a conventional loan without PMI. To do this, you'll demand at least xx percent equity in your home and a credit score of at to the lowest degree 620 or college. Y'all'll besides need to pay closing costs and consummate the new loan's underwriting process.

Does a Streamline Refinance bear upon your credit score?

A not-credit qualifying FHA Streamline Refinance Loan won't bear upon your credit score very much because your new loan balance will be about the same size equally your one-time loan balance. Since the FICO scoring model considers the age of your loans, you may lose a few points by replacing an older mortgage with a new mortgage. Just the effect tends to be minimal, especially if you've had your current loan only a few years. The credit-qualifying Streamline Refinance will cheque your credit score which could temporarily lower your score a little.

What are the cons of an FHA Streamline Refinance?

The FHA Streamline Refinance'due south biggest strength is its simplicity. But that could also be seen as its greatest weakness. Because you're skipping the dwelling house appraisement, and the credit qualifying process in many cases, you lot tin't increment your loan amount to get cash back. Some other con: You lot can't refinance out of paying mortgage insurance like you tin with a conventional loan.

How long does an FHA Streamline Refinance take?

The FHA Streamline Refinance skips the dwelling appraisal. This means you could close on the loan almost a calendar week sooner than yous could with other refinance loans. Still, y'all'll probable need 4 to five weeks to close on the new loan.

Check your FHA Streamline eligibility

FHA mortgage rates are low and homeowners typically shut faster with a Streamline Refinance. Recall: the sooner you close, the bigger your FHA MIP refund.

Become started by checking today's FHA refinance rates to see what you could save.

The data contained on The Mortgage Reports website is for advisory purposes merely and is not an advertising for products offered past Full Beaker. The views and opinions expressed herein are those of the author and do not reverberate the policy or position of Full Chalice, its officers, parent, or affiliates.

espinosathantaight.blogspot.com

Source: https://themortgagereports.com/1604/fha-streamline-refinance-mip-refund

0 Response to "I Already Used Stremline Refinance Can I Do It Again"

Post a Comment